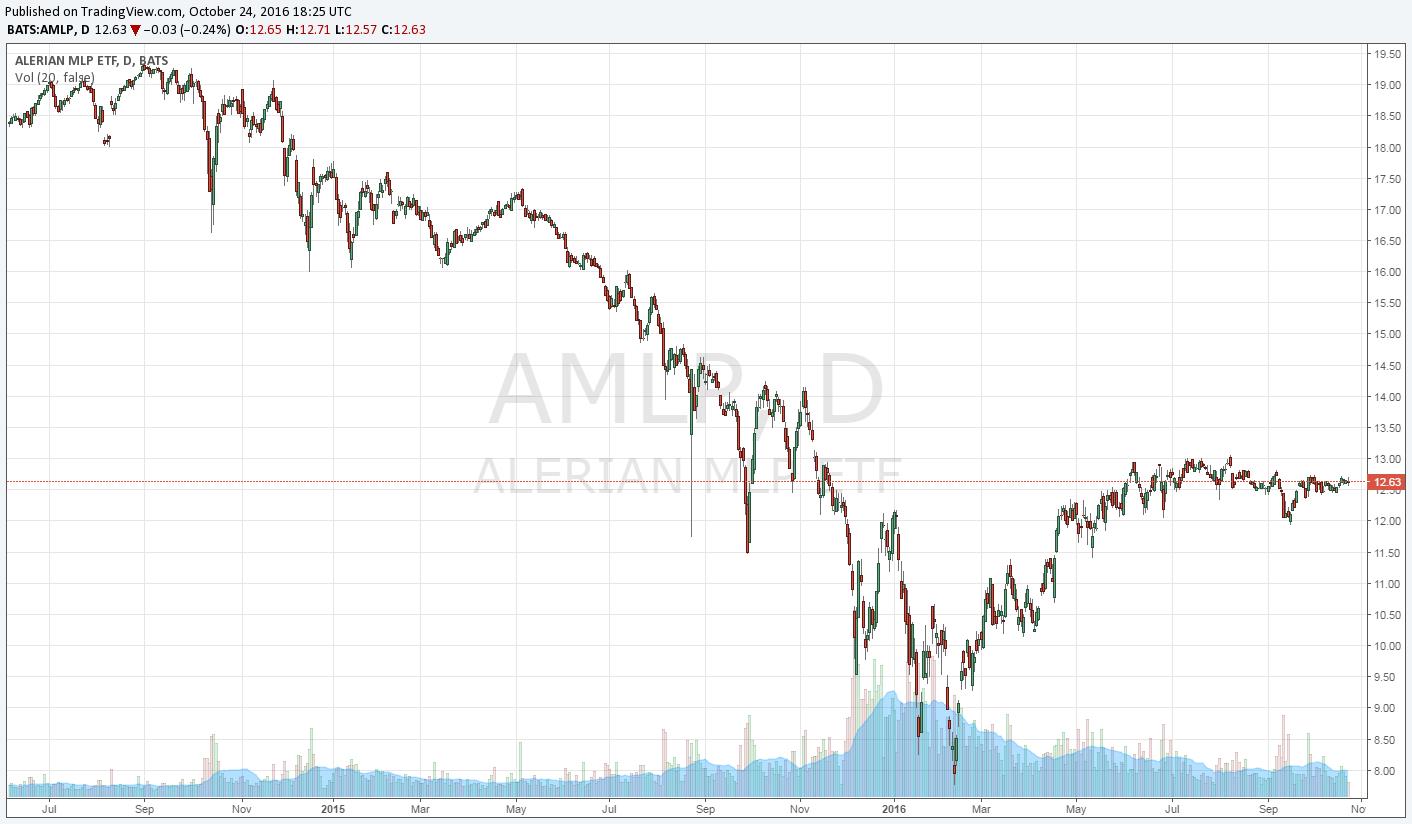

Image show above: Performance of the Alerian MLP ETF.

“Perhaps the worst thing about MLPs is that investors can spend more time doing and thinking about tax-related items than actually evaluating the businesses of the underlying entities. This could result in poor investment decisions.” – Brian Nelson, CFA

By Brian Nelson, CFA

What a sensitive topic for many…

Our team presented at the Chicago chapter of the American Association of Individual Investors (AAII) last weekend. It is always an honor and a privilege to have the opportunity to present to such wonderful people! They ask so many great questions. (By the way, I’m working on my schedule for 2017, so if you’d like our team to speak on a topic of interest at an event near you, please let me know. Be sure to send info about the event. I can be reached at brian@valuentum.com.)

On the way out after the Chicago AAII presentation, I was talking to a married couple. They reminded me of the many very disappointing tax issues that complicate the investment-decision-making process of master limited partnerships, or MLPs. Not only was the married couple disgusted by the poor performance of MLPs, as the chart above of the Alerian MLP Trust ETF (AMLP) from June 2014 through today shows, but the couple was even more disappointed by the tax bill that comes with owning these vehicles. It reminded me of a Journal article I read some time ago (Sanders, Laura: Thousands Hit With Surprise Tax Bill on Income in IRAs, November 13, 2015. Wall Street Journal):

“…investor Steve Goldston of Phoenix received a surprise tax bill for $24,321. It was for units of a master limited partnership affiliated with Kinder Morgan Inc. that Mr. Goldston held in his Roth individual retirement account. The total included nearly $6,000 of late-filing penalties and interest.

“I was outraged,” says Mr. Goldston. “Here was a tax form, completely filled out and signed on my behalf, saying that I owed this money and it was coming out of my IRA—but that was the first I heard.” …

…Thousands of investors holding MLPs in IRAs at other firms may owe similar taxes that they aren’t aware of, experts say.

The unexpected bills are painful reminders that even widely held investments such as MLPs can contain tax traps, experts say.”

Our team spends most of its time thinking about how we can help investors of all types. The rest of the time is spent putting those thoughts into practice.

For those that were members to Valuentum prior to June 2015, before we sent out our far-reaching transaction alert email on Kinder Morgan (KMI) and the midstream energy MLP space, more broadly, it’s very easy to see how valuable our service is (I sincerely hope our genuineness has shown through). For those that joined when we received widespread publicity on our call on Kinder Morgan and the midstream energy MLP space in Barron’s and elsewhere on our about late 2015/early 2016, it may not be as easy to see, unfortunately.

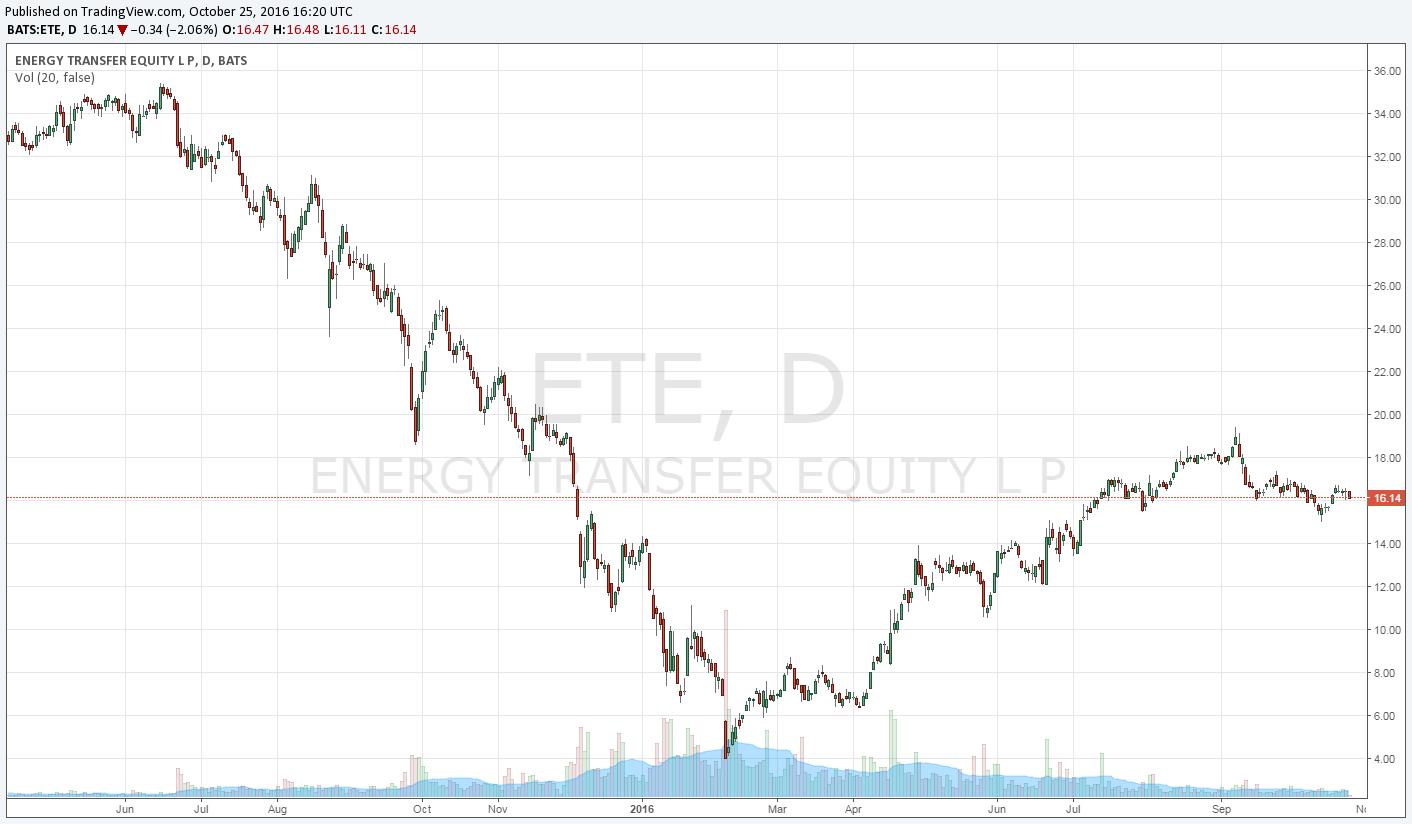

Units of master limited partnerships have bounced from what I would describe to be a “panic-selling bottom” in early 2016 and are now down only about one third from their all-time peak set in the summer of 2014. Energy Transfer Equity (ETE), for example, fell to ~$4 from ~$35 in June 2015, but the entity has rallied back to the mid-teens, now a 50% decline from its peak (about the time we sent out our warning email). It’s been a wild ride…but still a flat-out ridiculous one for income vehicles, would you say?

Image show above: Performance of Energy Transfer Equity (ETE).

As the married coupled noted, however, the pain of witnessing the prices of MLP units collapse is only half of the story for investors. The tax situation made things even worse. From that Journal article:

“Under the tax code, IRAs and Roth IRAs have significant benefits—such as tax-free growth—but they come with limits. When owners use IRA funds to invest in partnerships, as opposed to stocks, bonds and funds, they owe tax on certain annual income from the partnership exceeding $1,000 because of an antiabuse provision. This levy is known as Unrelated Business Income Tax, or UBIT, and its top rate of 39.6% can take effect at about $12,000 of taxable income.

A further, unique twist is that when this tax is due, the IRA custodian or trustee—such as Pershing or Charles Schwab (SCHW)—is responsible for obtaining a special tax ID number and then filing and signing an IRS Form 990-T reporting the income. The IRA owner is typically responsible for paying the tax.

Because of this complexity, experts often caution investors to avoid putting publicly traded partnerships into IRAs.”

I think one of the more convoluted dynamics of MLPs is the “return of capital” component of their structure, and how that impacts their tax treatment for the individual unitholder, outside tax-shielded accounts. MLPs do not pay traditional dividends, per se, but issue what’s called tax-deferred distributions, with the distribution, or part of it, reducing an investor’s cost basis in the unit over time. Tax implications typically occur when the unit is sold, and only through death can a unitholder avoid prior-distribution taxation as the basis is reset to the market price when units are passed to heirs.

With the sharp price declines across the MLP universe as of late, even for investors that have held MLPs for a very long time, the tax benefits may be hard to come by. Because of the return-of-capital impact that lowers an investor’s cost basis in MLPs, even if an investor sells at a price substantially lower than the price of their original purchase, they could still be on the hook for a taxable gain. It’s complicated, to say the least.

But what’s potentially worse is the idea that many holders of MLPs may have sought out these vehicles solely because of their tax advantages on the income stream, only to find today that they are holding something they may not like, if now only to take advantage of the long-term capital gains benefit, if or when the cost basis reaches $0. In my humble opinion, if the decision is made before one purchases something to hold it for a long time, just for tax reasons, that decision is not really “investing,” which instead is based on the value of a business’ assets relative to the price at which they can be purchased.

I wonder if the US tax system, in part, had something to do with the inflating of the MLP bubble prior to the collapse in June 2015. Were investors letting the tax-implications “tail” wag the business-value-question “dog, thereby creating an irrational marketplace at the peak? It is certainly up for debate.

In any case, one has to have a savvy tax attorney, financial advisor, and financial analyst to figure out whether MLPs are right for them, let alone get comfortable and be knowledgeable about the entire opportunity. But even so, after one considers the performance of the MLP universe following the June 2015 collapse and the eroding tax benefits that may come from the “return of capital” proposition, the reasons for owning MLPs aren’t as clear as the companies that issue such units may want you to believe. In my humble opinion, MLPs may very well be “financial instruments of mass destruction,” to borrow a phrase from the Oracle’s opinion on derivatives.

Please be sure to check with your tax attorney and financial advisor. This note is by no means tax or financial advice in any way, shape or form, and your mileage may certainly differ. Now read, “Are MLP Structures Phony (login required).”

Pipelines – Oil & Gas: BPL, BWP, DPM, ENB, EPD, ETP, EVEP, HEP, KMI, MMP, NS, OKS, PAA, SE, SEP, WES

Tickerized for various MLPs across the energy space.