By Brian Nelson, CFA

I tread very lightly in how I communicate broad macroeconomic information. There are investors that are purely macro-focused asset-allocators, there are eternal optimists that believe the sky is the limit regardless of any economic considerations (perhaps like the Oracle of Omaha these days?) and then there are legends like Peter Lynch who is attributed with saying that “if you spend more than 13 minutes analyzing economic and market forecasts, you’ve wasted 10 minutes,” and that “if all the economists in the world were laid end to end, it wouldn’t be a bad thing.” Peter Lynch was the manager of the Fidelity Magellan Fund that averaged a near-30% annual return during the 13-year period ending 1990, “You Loved This One: A Little Inspiration.”

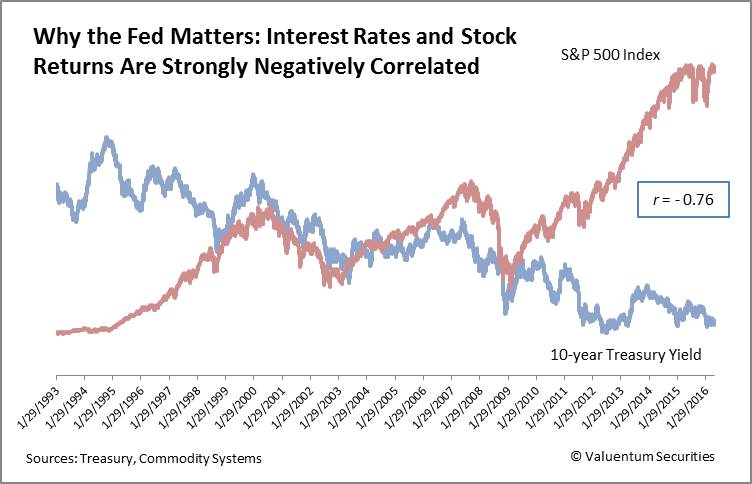

I’ve welcomed the idea of not putting too much weight in near-term macro trends, much like that of the school of Buffett, but where I do spend particularly close attention to macro dynamics is in the case of “outlier-type” events like that of the Financial Crisis in 2008/9 or in the case of the existing environment today, where valuations on S&P 500 stocks are stretched, “Soros, Icahn, Nelson Hedge for Market Fall (May 2016),” and the market is staring down the onset of contractionary monetary policy, which while easy to dismiss as mere headline noise, is very important. When it comes to almighty interest rates, they are a key focal point in stock valuation analysis (i.e. a key driver behind intrinsic value) and by extension potential stock returns. The value of future free cash flows generated 10 or 15 years in the future, for example, is substantially more in an interest rate environment of near-0% than one of, let’s say, 5% or 10%. Interest rates matter to stock valuations – and historical data analysis implies a very strong negative correlation between rates and stock returns in part because of this very reason.

Though others have their reasons, the primary reason I pay attention to Fed activity is fundamentally-based and tied to the discount rates used within our discounted cash-flow valuation process. To us, the Fed matters – what they do with rates matters, and because of this, we can’t ignore the news flow. On May 18, the markets received the Fed minutes for the April 26-27 meeting, and while meeting participants continue to reveal caution and prudence in the statement, the likelihood of a rate hike in 2016 has increased considerably and from what I can gather may happen as early as June (page 9/10). I’ve provided an excerpt of the minutes below and have bolded a few sentences that I think are rather telling of a more hawkish Federal Reserve.

Some participants saw limited costs to maintaining a patient posture at this meeting but noted the risks—including potential risks to financial stability—of waiting too long to resume the process of removing policy accommodation, especially given the lags with which monetary policy affects the economy. A couple of participants were concerned that further postponement of action to raise the federal funds rate might confuse the public about the economic considerations that influence the Committee’s policy decisions and potentially erode the Committee’s credibility.

A few participants judged it appropriate to increase the target range for the federal funds rate at this meeting, citing their assessments that downside risks associated with global economic and financial developments had diminished substantially since early this year, that labor market conditions were consistent with the Committee’s maximum-employment objective, and that inflation was likely to rise this year toward the Committee’s 2 percent objective. Two participants noted that several standard policy benchmarks, such as a number of interest rate rules and some measures of the equilibrium real interest rate, continued to imply values for the federal funds rate well above the current target range. Such large and persistent deviations of the federal funds rate from these benchmarks, in their view, posed a risk that the removal of policy accommodation was proceeding too slowly and that the Committee might, in the future, find it necessary to raise the federal funds rate quickly to combat inflation pressures, potentially unduly disrupting economic or financial activity. Overly accommodative policy could also induce imprudent risk-taking in financial markets, posing additional risks to achieving the Committee’s goals in the future.

Participants agreed that their ongoing assessments of the data and other incoming information, as well as the implications for the outlook, would determine the timing and pace of future adjustments to the stance of monetary policy. Most participants judged that if incoming data were consistent with economic growth picking up in the second quarter, labor market conditions continuing to strengthen, and inflation making progress toward the Committee’s 2 percent objective, then it likely would be appropriate for the Committee to increase the target range for the federal funds rate in June. Participants expressed a range of views about the likelihood that incoming information would make it appropriate to adjust the stance of policy at the time of the next meeting. Several participants were concerned that the incoming information might not provide sufficiently clear signals to determine by mid-June whether an increase in the target range for the federal funds rate would be warranted. Some participants expressed more confidence that incoming data would prove broadly consistent with economic conditions that would make an increase in the target range in June appropriate. Some participants were concerned that market participants may not have properly assessed the likelihood of an increase in the target range at the June meeting, and they emphasized the importance of communicating clearly over the intermeeting period how the Committee intends to respond to economic and financial developments.

There’s no need to panic when it comes to contractionary monetary policy, but readers should be cognizant of what it implies. For starters, within the stock valuation context, longer-duration free cash flows are worth less, and that means equity valuations will be reset lower over time, an effect opposite of that witnessed in the chart above as the 10-year Treasury yield (eventually) rises instead of falls (1993-2016). Second, we talk a lot about the “yield tipping point” or the point at which the yield on a riskless asset such as that of a Treasury bill eventually becomes more than that on most dividend-paying risky assets, theoretically prompting asset flight away from income-growth equities into higher-yielding fixed income instruments (think market sell-off). This dynamic may not happen anytime soon, but it’s something to be aware of. If you haven’t read our ‘5 Concerns About Impending Rate Hikes (January 2016),” it may be worth revisiting. We’re not making any changes to the newsletter portfolios as a result of the incrementally more hawkish stance by the Fed.

Broad Market ETFs: SPY, DIA

Related ETFs: TBT, TLT, TMV, IEF, TBF, EDV, TMF, PST, TTT, ZROZ, VGLT, TLH, SBND, IEI, TYO, UBT, UST, DLBS, DTYS, TLO, VGIT, TBX, SCHR, ITE, GSY, LBND, TYD, DTYL, VUSTX, DLBL, TYBS, DFVL, TBZ, DFVS, TYNS